Portfolio balance

Drew O’Neil discusses fixed income market conditions and offers insight for bond investors.

Stocks and bonds can each play a role in a portfolio. Neither is necessarily better or worse… they are just different. Owning a share of stock means that you own a piece of the entity. Owning a bond means that you are lending money to the entity. When you own a piece of a company, you hope that the company becomes more valuable over time and your share correspondingly increases in value. If you loan money to a company, you want the company to pay you the interest that they owe you and then pay off the loan at the end of its term. Equities generally come with the potential for large gains and can be a good option for the growth portion of your portfolio. Bonds generally have a lower potential for large gains, yet because their returns depend on an entity making interest and principal payments (not growth), they can be a good option for the wealth preservation portion of your portfolio.

As humans, we are prone to succumb to recency bias when contemplating the future. Given that we just closed the books on a third consecutive year of positive equity gains, many investors are feeling quite optimistic about the potential for continued strong equity market performance. While this is a possibility, so is the opposite. Should we experience a rough patch in the equity markets in the near future, is your portfolio positioned in such a way that the potential volatility will let you remain calm and your financial journey remain on track?

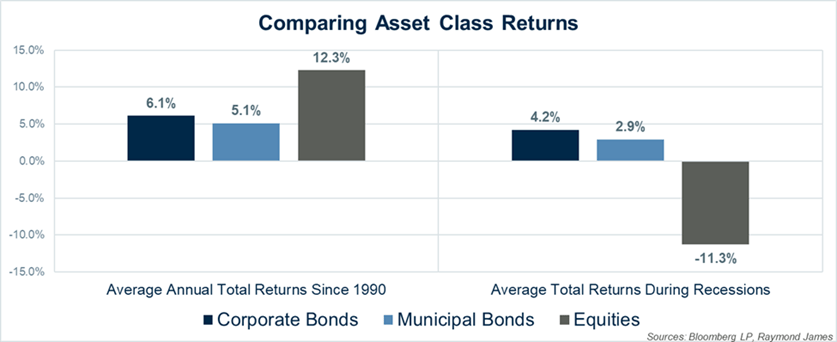

In an attempt to overcome our inherent recency bias, the chart above hopefully serves as a reminder that the stock market does not always go up. The left side of the chart shows the average annual returns since 1990 of corporate bonds, municipal bonds, and equities. Fixed income has performed well but lags the growth in the equity market, as would be expected. The right side of the chart shows what investors should be prepared for, even if a recession is not expected in the near term: average returns during recessions over the same timeframe. While lower than non-recessionary periods, fixed income performance remained solidly positive on average even during recessions. Equity market performance tells a different story, averaging negative 11.3% during recessions.

Is your current portfolio allocation aligned with a potential level of volatility that you are comfortable with? Or, like many investors, has your equity allocation expanded beyond where it should be given your risk profile? As we kick off 2026, now is a good time to reassess your overall portfolio allocation to ensure it hasn’t drifted too far off target given the strong equity performance over the past three years. Yields across the fixed income space remain elevated relative to recent history. This means that investors can rebalance their portfolio by capturing equity gains and shifting those gains into the wealth preservation portion of their portfolio, while locking in attractive yields for years to come with individual bonds.

The author of this material is a Trader in the Fixed Income Department of Raymond James & Associates (RJA), and is not an Analyst. Any opinions expressed may differ from opinions expressed by other departments of RJA, including our Equity Research Department, and are subject to change without notice. The data and information contained herein was obtained from sources considered to be reliable, but RJA does not guarantee its accuracy and/or completeness. Neither the information nor any opinions expressed constitute a solicitation for the purchase or sale of any security referred to herein. This material may include analysis of sectors, securities and/or derivatives that RJA may have positions, long or short, held proprietarily. RJA or its affiliates may execute transactions which may not be consistent with the report’s conclusions. RJA may also have performed investment banking services for the issuers of such securities. Investors should discuss the risks inherent in bonds with their Raymond James Financial Advisor. Risks include, but are not limited to, changes in interest rates, liquidity, credit quality, volatility, and duration. Past performance is no assurance of future results.

Investment products are: not deposits, not FDIC/NCUA insured, not insured by any government agency, not bank guaranteed, subject to risk and may lose value.

To learn more about the risks and rewards of investing in fixed income, access the Financial Industry Regulatory Authority’s website at finra.org/investors/learn-to-invest/types-investments/bonds and the Municipal Securities Rulemaking Board’s (MSRB) Electronic Municipal Market Access System (EMMA) at emma.msrb.org.